Stress-tested against four market regimes.

Monte Carlo validation that bootstraps from the same historical window can only stress-test with the fat tails that window already contained. The cGAN, trained on four distinct real SPY regimes, generates unlimited synthetic paths that preserve regime-specific volatility clustering and tail behavior.

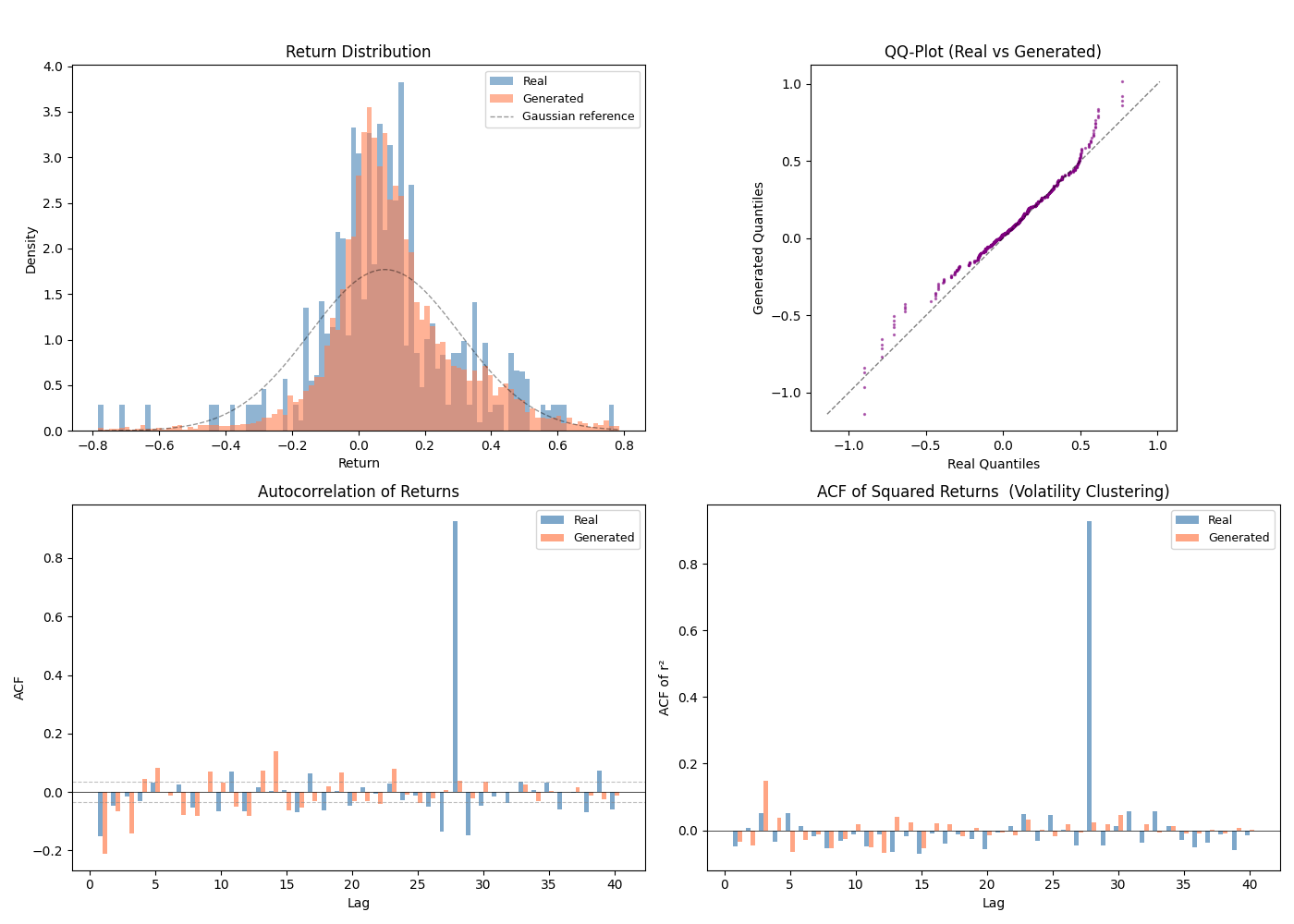

The properties the GAN preserves.

Volatility clustering. Autocorrelation of squared returns matches real data (verified via ACF plots). Bootstrapped blocks break clustering at block boundaries.

Fat tails. Excess kurtosis is preserved per regime, not washed out by averaging across market environments.

Regime conditioning. Ask the model for a thousand crash scenarios and it generates paths with COVID-like drawdown dynamics, not generic noise with a negative drift.

Honest caveats in Limitations §4: the crash regime has only 23 training windows, and the 252-bar paths shown here stitch together independent 30-step chunks — autocorrelation breaks every 30 bars.